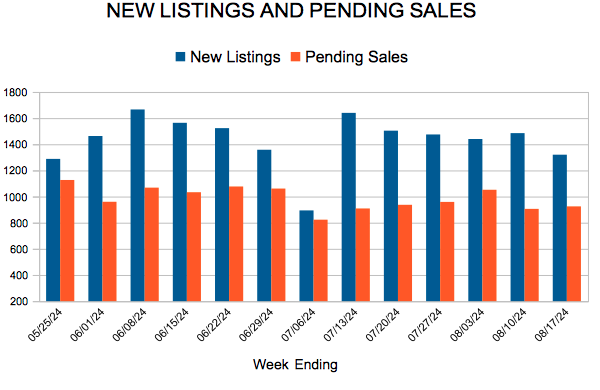

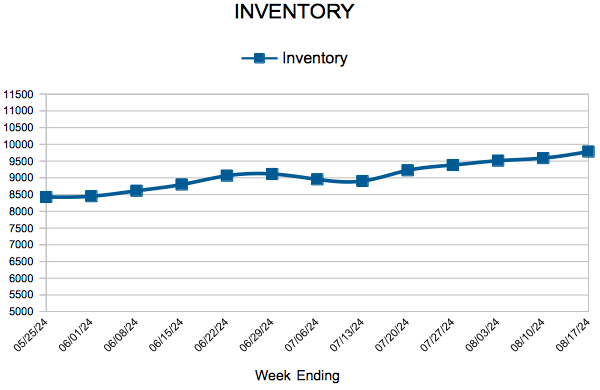

New Listings and Pending Sales

For Week Ending August 17, 2024

For Week Ending August 17, 2024

The number of homes for sale continues to improve nationwide, marking the ninth straight month of growth. According to Realtor.com’s July 2024 Monthly Housing Market Trends Report, there were 36.6% more homes on the market in July compared to the same period last year. Prospective buyers, especially first-time homebuyers, will be pleased to know the growth in homes priced between $200,000 – $350,000 jumped 47.3% year-over-year, outpacing all other price categories.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING AUGUST 17:

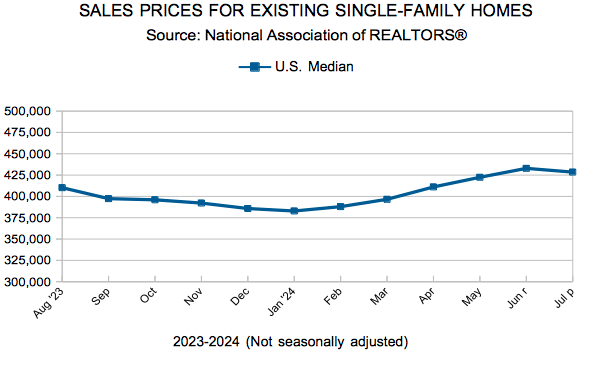

FOR THE MONTH OF JULY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

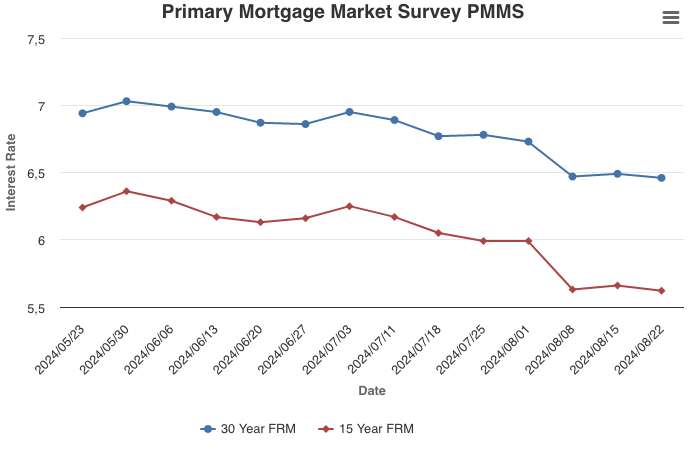

August 22, 2024

Although mortgage rates have stayed relatively flat over the past couple of weeks, softer incoming economic data suggest rates will gently slope downward through the end of the year. Earlier this month, rates plunged and are now lingering just under 6.5 percent, which has not been enough to motivate potential homebuyers. Rates likely will need to decline another percentage point to generate buyer demand.

Information provided by Freddie Mac.