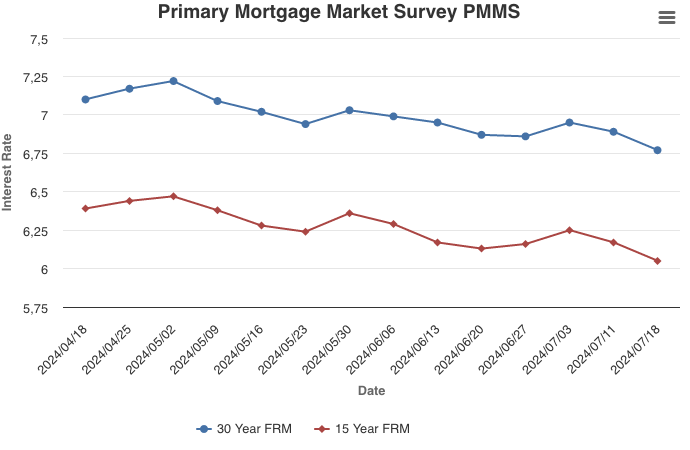

For Week Ending July 13, 2024

For Week Ending July 13, 2024

U.S. homeowners with a mortgage saw their equity increase 9.6% year-over-year in the first quarter of 2024, an average gain of $28,000 and the highest number since 2022, according to CoreLogic’s Homeowner Equity Insights report. At the state level, California saw the greatest equity gain at an average of $64,000 annually, followed by Massachusetts and New Jersey, at $61,000 and $59,000, respectively.

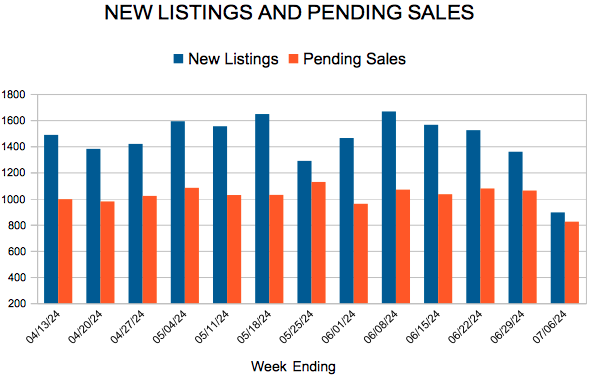

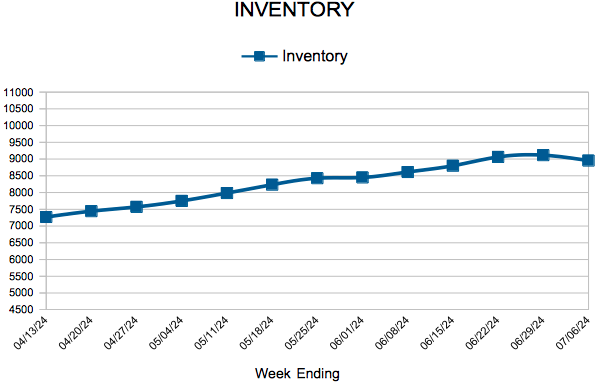

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING JULY 13:

- New Listings increased 4.8% to 1,640

- Pending Sales decreased 15.4% to 909

- Inventory increased 10.3% to 8,905

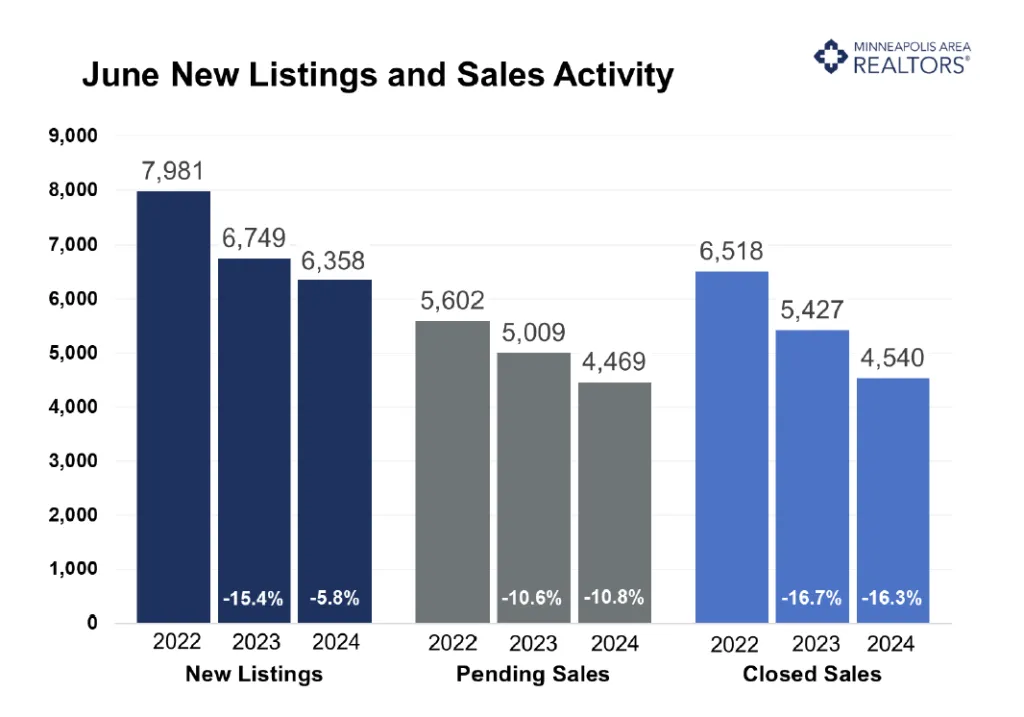

FOR THE MONTH OF JUNE:

- Median Sales Price increased 1.8% to $390,000

- Days on Market increased 9.7% to 34

- Percent of Original List Price Received decreased 1.2% to 100.1%

- Months Supply of Homes For Sale increased 14.3% to 2.4

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.