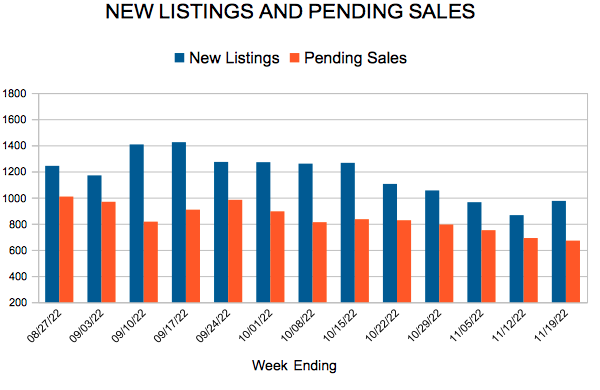

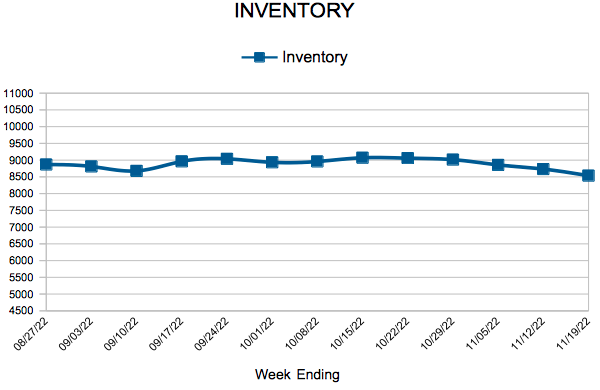

New Listings and Pending Sales

For Week Ending November 26, 2022

For Week Ending November 26, 2022

The share of first-time homebuyers has fallen to an all-time low, with first-time buyers making up 26% of all buyers for the fiscal year ending June 2022, while the age of the typical first-time buyer increased to 36 years old, an all-time high, according to the National Association of REALTORS® Profile of Home Buyers and Sellers, which has been published since 1981. Higher borrowing costs and a lack of affordable housing have forced many buyers out of the market this year, and inflation and rising rents have made it more difficult to save up for a down payment.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING NOVEMBER 26:

FOR THE MONTH OF OCTOBER:

All comparisons are to 2021

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

December 1, 2022

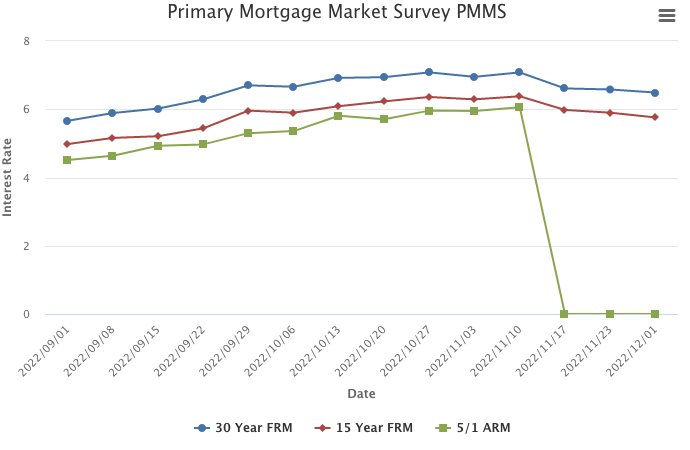

Mortgage rates continued to drop this week as optimism grows around the prospect that the Federal Reserve will slow its pace of rate hikes. Even as rates decrease and house prices soften, economic uncertainty continues to limit homebuyer demand as we enter the last month of the year.

Information provided by Freddie Mac.